Not content with nearly tanking the economy with their

mini-budget, the Truss government has another little problem with tanks, or

rather the lack of them. I’m talking about gas tanks.

Gas storage

Back to the 1970s?

Half a century ago, when Tory Edward Heath was Prime

Minister, the country was in turmoil with strikes and protests. One such strike

was by the coal miners, at a time when (UK-mined) coal was by far the largest source

of energy for electricity generation. People of my age remember the 3-day week accompanied

by rolling 3-hour power cuts. The underlying problem was that electricity

generators had run down their stockpiles of coal and so put themselves (and the

country) in a vulnerable position when the miners went on strike.

Heath called a “who runs Britain?”-themed general election.

The voters’ reply was “not you” and Harold Wilson (Labour) became Prime

Minister in a hung parliament. Wilson subsequently awarded the miners a 35% pay

rise.

You may be thinking: nothing like this could happen now?

Well, obviously no-one (except possibly bankers) would get a

35% pay rise and the top 1% of earners would never settle for so little. But

there are some similarities…

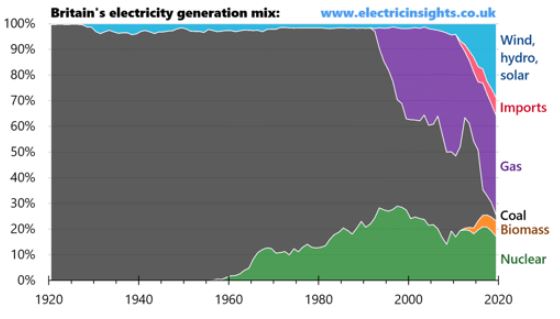

50 years of electricity generation

Reports in the last 24 hours warn that, in a realistic worst

case scenario, rolling 3-hour power cuts may be returning to Britain this

winter. So what has changed in the past 50 years?

Electricity sources

This graph (which covers the last 100 years) shows

that, in the 1920s, all our electricity was generated by coal. At the time of

the 3-day week, nuclear and a small amount of hydro power had made some

incursions, together representing about 10-12% of electricity generated. So the

miners still held enormous power over our electricity needs.

The really big changes have occurred in the last 30 years. In the 1990s, gas started to make big inroads into the dependence on coal (the latter by now all imported) and nuclear rose steadily over the 40 years from 1960. The past 10 years has seen a dramatic rise in renewables (wind and solar) and coal has now all but disappeared from the mix. Renewables now account for around 30% of electricity generated, the big rise being mainly in offshore wind. The much cheaper onshore wind saw its rise dramatically halted in 2015 by Tory changes to planning rules and NIMBY local authorities. It’s interesting to note that direct electricity imports (by cable), although still small, only feature in the mix from around 12 years ago. (Biomass remains controversial, with sharply differing opinions as to whether or not it can be considered “green”. I think not.)

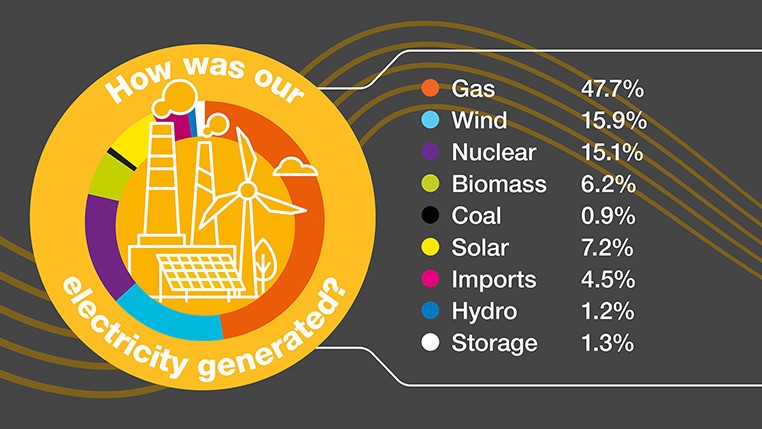

Out of power

Our current mix of electricity generation looks like this

(figures for August 2022):

Current electricity sources

Gas still dominates: nearly half our electricity comes from

gas, which is why it features strongly in the energy price. Coal has all but

disappeared, but may make an unwelcome comeback to get us through the winter. “True”

renewables (wind, solar, hydro) make up about a quarter, nuclear around 15% –

and note that imports account for about 5%.

The government is correct to identify the Russian withdrawal

of gas from world markets as the biggest disruptive effect to global gas

supply. We import around 60% of our gas consumption (as both a fuel and for

electricity generation) and export around 20%.

But there are 3 areas in which the UK has shot itself in the

foot:

As already mentioned, a much faster rollout of

onshore wind – the cheapest source of electricity – would have left us far less

dependent on fossil fuels, benefiting both imports and CO2 emissions.

The UK has some of the most badly

insulated houses in Europe. Government policies and schemes have gone

through some bewildering changes and budget reductions in the past decade or

so. A more consistent and generous national scheme over the past few years

would have brought a double benefit. Households would have warmer homes and

lower energy bills. The country would use less gas.

Last, and not least, the UK made a bad strategic

decision in 2017 to allow Centrica to close the country’s biggest gas storage

facility. This decision has been recently

reversed but the country was warned at the time that the closure exposes

the UK to more volatile gas prices and a likely higher dependence on

imported hydrocarbons. Sounds familiar?

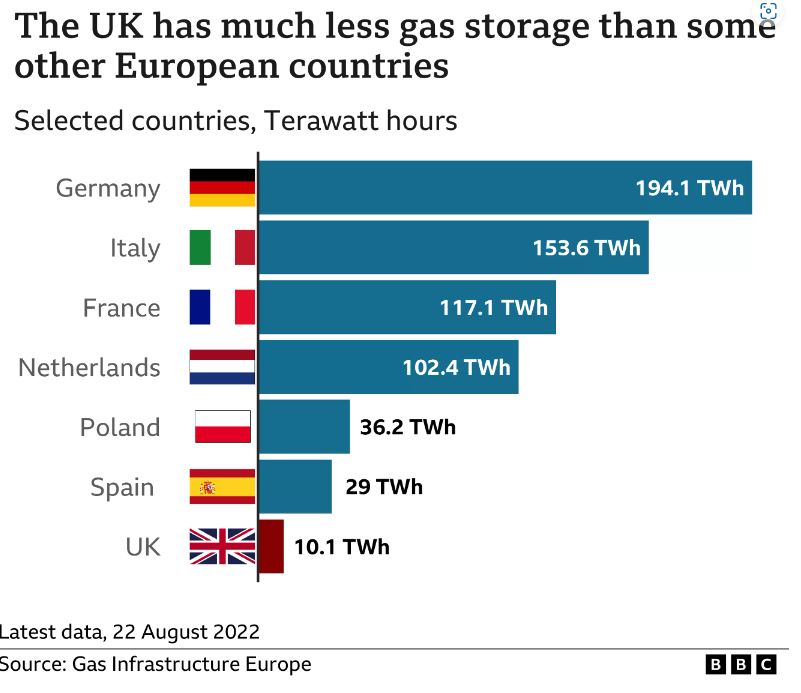

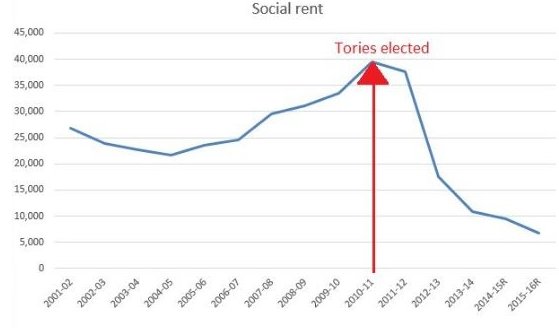

Gas storage capacity

EU countries with ample gas storage facilities have been

filling these over the summer months to provide a buffer stock for the winter.

Currently, gas

stored across the EU is at 90.4% of capacity, representing just over 3

months’ demand. By contrast, the UK’s tiny storage facility is 99% full, representing

just four and a half days’ demand.

Go figure. And they say history does not repeat itself.

Sometimes nowadays it seems that reality has been replaced by a dark, dystopian satire. The old phrase “you couldn’t make it up!” would apply so often that we don’t give it another thought.

“Don’t Care” Rooms

The news that prompted my musings was that of an Essex hospital that was giving serious consideration to going into partnership with a company called CareRooms. In an apparently innovative way to reduce the problem of “bed-blocking” patients ready for discharge, but needing ongoing care and support, would move to spare rooms in private homes. The company would provide a form of brokering service, matching room providers to patients. Prospective hosts were said to be able to earn “up to £1000” a month.

Initial reaction from some quarters was positive. Some even suggested this would be a means for some hosts on benefits to avoid the “bedroom tax”. Income for householders, earlier release from hospital for patients, reduced benefits bill: what’s not to like? Everyone’s a winner, are they not? Y-e-e-s, well, hang on a minute…

All you need?

Before the NHS was set up in 1948, the misery and suffering by poor people because of a lack of affordable healthcare was a national – and international – scandal. They would avoid or delay seeking medical care because of the costs. Decisions such as “shall I call the doctor or feed the kids?” were commonplace. Or “pay the rent”, “light a fire”, “replace my worn-out shoes” and many, many more. The NHS was set up so that “never again” would people face these agonising choices. It was, and remains, a testament to the compassionate side of our human nature.

For the reasons just stated, it would have been literally unthinkable to suggest such a get-rich-quick scheme. For householders to provide care, and for the intermediary company to profit from, a service which should available, as of right, to all, defies the very founding principles of the NHS.

It’s wrong for several other reasons, too. Firstly, it’s just a way to try to get around the chronic underfunding of the NHS. For too long, we’ve tried to get our healthcare on the cheap. Secondly, it tries to solve the wrong problem. True, shortage of beds is one of the consequences of the underfunding, as one of the graphs from the last link shows. But the bigger problem is the shortage of properly trained community care staff to care for those discharged from hospital safely and appropriately. The people concerned are disproportionately vulnerable and elderly. How many of us would want an elderly relative – or ourselves – looked after by a well-meaning amateur who may have been attracted to the scheme by the money to be made?

The hospital quickly dropped the idea once it got publicity and a hostile reaction. But the fact that it was considered is an example of what I call the “marketization of thought”.

Our Factory Universities

Another example of how market thinking has spilled over into other human activities is how we discuss policy about universities. In my student days, it was natural to think of education, per se, as a “good thing”. More (good quality) education was even better and as many of us as possible should enjoy as much of it as possible. It wasn’t just the opportunity to learn things, of course. It was also very much about the process of learning: the new skills developed: to challenge and be challenged, to refine an idea reflectively or collectively, to create new ways of seeing things. We took for granted that all this experience would lead naturally to a better society: better informed, more highly skilled people making better decisions. Reason, rational debate and mutual respect were all part of this essentially Enlightened idea.

University factory

Depressingly, universities seem to be treated more and more as factories: factories which are there to enhance the lifetime earning powers of its products: the students. Certainly the whole debate about student loans is conducted in these terms. Individuals benefit, of course – the material self-interest mantra at the heart of Free Market Fundamentalism – and it is also sold as benefiting “UK plc”, whatever the hell that is. Oh yes, it’s the reduction of all our plans, our hopes, dreams, loves and fears, smiles and tears to the sum total of all the transactions in the land.

The “Customer Service” Nightmare Experience

Marketization of thought affects the way we, as consumers, interact with those from who we buy goods and services. Customer service has become increasingly impersonal. Consumers are encouraged more and more to use online services, requiring no real-time human interaction. For a large range of goods and services, this works pretty well for purchases, and when coupled with delivery to your door, is often far more convenient than a visit to the shops.

The old ways weren’t perfect. I remember, as a child, being dragged from shop to shop by my mum on a seemingly endless round of activity, but often not much seemed to get bought. My memory is of wasted hours in and out of the cold and coming home empty-handed. But every one of those would-be purchases would involve a face-to-face conversation, in naturalistic language, where preferences and nuances of taste could be mediated. There was a bit of polite social chit-chat, too – usually about the weather.

The range and quality of goods on offer has improved beyond my wildest childhood imaginings. Product innovation is an area where markets do serve us well. But, even here, some new product or service probably sits on the shoulders of an innovative breakthrough enabled, and publicly funded by those universities of which I spoke earlier.

But woe betides you when things go wrong. In 21st century Britain, so-called “customer service” too often takes the form of a Kafkaesque nightmare. Firstly, the company website: before you can begin to find how you can get help, you wade through a sea of “FAQs”, arranged in some arbitrary, illogical order, none of which seem to address quite your problem. Next, the “Contact us” page, often presented with just the wrong set of questions to “steer” you to the right department. These pages often have helpful message boxes to fill in, which sends an email to some unknown destination deep in the bowels of the organisation – but you don’t know where because there’s no fucking email address to be seen! And the number of times I’ve searched a website in vain for a contact phone number for myself or on behalf of clients, in my role as an adviser: yes, Virgin Media, that does include you!

Don’t Call Me

Please press 1 to give up!

Which brings us to that most vexed of subjects: the call centre. The consumer organisation Which? once reported that waiting times on customer service phone numbers are, on average, seven times longer than those for sales departments. No, it wasn’t you’re imagination. And I cannot begin to count the hours I’ve spent listening to the Four Seasons on DWP and other government department call centre lines. If Vivaldi were still alive, his royalties would easily make him the richest man on the planet! Once you’ve navigated the “Press 1 for…, press 2 for…” hurdles, listened patiently to music on hold, you eventually reach an operative reading from a script who doesn’t have the authority to solve your problem. They promise to get “someone” to ring you back, but…

I had an early inkling of this “painting by numbers” approach to customer service when on a family holiday in the USA about 30 years ago. With youngish children, we typically ate at “family” restaurants. I quickly spotted the routine: a young waitress – it was invariably a “she” – would mechanically go through lists of choices: fruit juices, how you like your eggs (I once said “fried” on my first visit to the States years earlier – and was given a look as if I were a complete idiot). The most bewildering list was for salad dressings: I remember “French”, which was nothing like anything I’d seen in France, and some brightly-coloured goo called “Thousand Island”. Where on earth were these thousand islands where they ate this gunk? Bored with listening to the same lists endlessly repeated day after day, I tried to take the initiative by pre-empting my choices. Big mistake! I soon learnt that, whenever I did this, my waitress got confused and I got the wrong order. I soon learnt to wait to be processed through the system.

It wasn’t the waitresses’ fault – or the call centre operators’ fault, or any of the other bored employees you actually spoke to. After all, they’d been given just enough training and authority to guide customers through a standardised corporate process, but not enough to interact as one human being with another. Clever people in corporate HQs would streamline everything for maximum efficiency – and profit. Pity the poor customer who doesn’t like being processed like an item on a production line.

And so it has become more generally in the world of “customer service”. All this only becomes possible when decision-making is centralised and customers are treated as economic units to be exploited, rather than living, breathing humans.

Interlude: A German Joke

Time to lighten the mood. This story dates from the late 1970s, long before the wonders of computer-aided design had enabled the sophisticated customization and flexibility of modern production process. It’s a joke told to me by the German delegate at an international conference I attended. He was anxious to prove that his compatriots do have a sense of humour. You’ll see the relevance – it goes like this:

Word had spread the length and breadth of Germany of an exciting new invention: The Wonderful, Amazing, Universal Shaving Machine. Its inventor was the blacksmith in a small, hilltop village in Bavaria – let’s call it Rasiersdorf for now – who had shown no particular skills before, apart from being a steady and reliable blacksmith. A coachload of interested tourists went to track down the inventor and his amazing machine. The blacksmith was a shy, self-deprecating man who led his group of visitors into his workshop.

“My Wonderful, Amazing, Universal Shaving Machine will give the perfect shave to any man in the village!” The tourists looked doubtful, so the blacksmith said: “Bring me any man in the village old enough to grow a beard!” The guide went and returned with the village butcher. He sat in the blacksmith’s chair and was tied in with a leather strap. The Wonderful, Amazing, Universal Shaving Machine was lifted up by the blacksmith and tied to the butcher’s head. Various leather straps were adjusted and then the machine was switched on.

Cogs of all sizes began to turn and whir and, sure enough, two minutes later, the butcher stood up, showing off his perfectly-executed shave. “That’s truly amazing!” the visitors cried. “Especially so”, said one, “considering all the different sizes and shapes of men’s heads and jawbones!”. “Ah, yes”, said the blacksmith, “But that was before the invention of the Wonderful, Amazing, Universal Shaving Machine!”.

Something for the weekend, sir?

The next time you’re waiting for a call centre to answer, you’re on to your third tune of music on hold, the seventh time you’ve been told by a recording that “your business is important to us” and they’re “experiencing unexpectedly high call volumes”, just think on my little tale. It might just help you to retain a little vestige of the will to live.

Market Overreach

I’ve written before about the problems that arise when markets overreach themselves into areas where they don’t belong, most notably in Cat and Mouse. Obvious areas are privatised water, the utilities and railways. Plus, of course, the NHS. The energy regulator, Ofgem, proved once again yesterday that it doesn’t understand the stupidity of what it is trying to regulate. It says that the “big six” oligopolistic companies made a healthy profit margin of 4.5% by overcharging those customers who had not switched suppliers. The gap between the lowest and highest tariffs has widened. If all customers, and not just those switching, were on the best tariffs, the companies would have made a 6% loss instead.

Ofgem refers to non-switchers as “less-engaged consumers”. “Engaged”? ENGAGED?? Pardon me: I like to get engaged in a good discussion at a meeting or a pub. I got engaged to each of my wives (serially!) before we got married. I also enjoy being engaged in the plot and characters of a well-crafted film, novel or TV series. People get engaged in sport, hobbies and pastimes they enjoy. But engaged in shopping around for where to buy the stuff that makes my light come on when I press the switch? Come off it! I can think of at least 8 billion other things I’d rather be engaged in! Electricity, water and public transport are all basic essentials to modern life. I just expect them to be there and work, at a fair price. At the end of a rail journey, I don’t want to be told “Thank you for choosing to travel today by X”. (Fill in your own privatised, monopoly rail company at the X.) As if I had a choice! Nationalise the lot and sack the regulators, and let us get on with our lives in peace!

A guide to life?

In their very different ways, the examples I’ve given above reflect the overreach of markets into every corner of our lives. Worse too, it’s infecting the language we use and the way we describe activities that have (or should have) nothing to do with markets. As Nobel Prize-winning economist Joseph Stiglitz has said: markets, like toilets, both man-made inventions, are very useful in the right context. But no-one tries to run the whole of society on the basis of toilets. The same must be true for markets.

Nadine “Mad Nad” Dorries MP, fervent anti-choice campaigner and former “celebrity” jungle dweller, said on TV yesterday that Theresa May should sack Philip Hammond as the Treasury were being “too negative” about the UK’s leaving the EU.

Once upon a time, there was a pied piper. He lived in a small town on an island just off the coast of Eutopia. He spent his days quietly, mostly staying at home playing tunes on his pipe. Children would pass by his house and hear the music through the windows. The children talked to one another and, slowly, his music gained more fame.

The piper’s most treasured possession was a large gold watch, given to him by his grandfather. His grandfather told him that the watch was given to him by his own grandfather. Usually, the watch kept good time. The piper wound the watch every day, and all was well. But then the piper began to notice that the watch was not quite so good at keeping the time. He tapped it and shook it, but it did no good. He became more and more angry. The tunes he played on his pipe became louder and louder, and more children gathered to hear them. Their parents were a little worried, but they thought to themselves: “What harm can befall our children by listening to a piper and his music?”

One day, the piper was really mad about his gold watch. In his rage, he threw the watch to the ground. When he picked it up again, the piper saw that the glass was cracked and there was a small dent in the side. But, most importantly, the watch had stopped. The piper wound the watch. No ticking. He shook the watch. No ticking. He shook it harder, but it made no difference.

The Clockmaker

The pied piper was still angry – in fact, even angrier than before. “I must find a clockmaker to mend my watch”, he thought. So he went down the road to the clockmaker’s shop. He told the clockmaker that he had dropped the watch. The clockmaker examined it carefully. “I can mend the broken glass quite easily” he said. “And can you just bang the inside of the watch with a hammer to fix the dent?” asked the piper.

The clockmaker opened up the watch and looked inside. “I’m afraid it’s not a simple as that” he said. He showed the piper the inside of the watch. It was full of delicate, tiny wheels and levers. “All of these levers and wheels are connected together in a complex way. It looks like there’s been a lot of damage. Mending all the wheels and checking they work together properly will take lot of time and skill”. The piper looked angry and snatched the watch back. “Experts!” he muttered and stormed out of the shop.

“I don’t need that clockmaker!” thought the piper. “I’ll find someone else to fix it in a trice”. So he went all around the town asking for anyone who could help. Nobody said they could. At this, the piper grew angrier still. He went back home and picked up his pipe. He started playing, louder and more strangely than before. The children of the town heard the strange piping and started to gather outside the piper’s house.

The piper found that playing the strange tune in his house didn’t make him any less angry. “I know,” he thought, “I’ll go for a walk: that will calm me down!” So he opened the front door and went outside, taking his pipe with him. He started to walk down the street, heading for the highest cliffs on the island. All the time, he continued to play his strange tunes. The children started to follow him down the street. We all know how that story ends, don’t we, children?

At last! After 35 years of Free Market Fundamentalism hegemony, there are now clear signs that this sociopathic philosophy is finally in retreat. I’m basing these remarks in particular on the events of the past two weeks: the Labour and Conservative Party Conferences. What’s significant above all is Theresa May’s admission of the existence of market failure.

For too long – far, far too long – the logic and language of markets have been used to describe practically every human activity. Two extracts from an excellent article by Dawn Foster about housing in today’s Guardian illustrate my point. The first: “Leaving housing to the market prioritises profit over human experience and the right to shelter.” The second, quoting theologian Herbert McCabe: “There is something bizarre about the present popularity of the word ‘market’ as a metaphor for human society. Markets are surely a good and necessary part of living together, as are law courts and lavatories. But none of these are a useful model for what human society essentially is.” Indeed so.

Housing is a good example of market overreach. Something intangible, but very valuable, was lost to us when we started treating houses as investments, rather than the places where we live and build our lives. Worse, to rent, rather than to own, one’s home is seen as some kind of moral failure. Other obvious examples of overreach are the privatised utilities and railways: 80% favour renationalisation. Indeed, if they could find a way of doing it, the “true believers” in the Tory Party (including several Cabinet members) would privatise the very air we breathe. Then we could have a cartel of Tory Party-donating private companies overcharging us for every breath we take!

But it looks like the fightback has begun in earnest, and Free Market Fundamentalism is in retreat.

Labour in Brighton

Corbyn and McDonnell

And so to the Labour Party Conference. The buoyant mood in the packed conference hall reflected a feeling that times are changing. But the Party was still quite a lot of seats behind the Tories in the election, so word of caution is needed. Jeremy Corbyn and John McDonnell have been consistent for a long time with a coherent set of economic policies. Misbranded as leftist or Marxist, Labour’s economic policy would have been totally mainstream in 1970s Britain and would still look so in much of mainland Europe. But the growth in party membership, particularly amongst younger voters, would suggest these policies’ time has come again. Their balanced approach is, of course, in tune with what it means to be human, as I’ve said long ago.

Talk of Labour taking Britain back to the 1970s is ironic in one respect. Jacob Rees-Mogg , the darling of Tory Party activists (average age 71) , also wants to take us back to the 70s – the 1870s!

Tories in Manchester

The empty seats at the Conservative conference betrayed the fact that Labour now has six times the membership of the Tories – and increasingly youthful. And the rows of grey-haired, bored-looking Tory delegates for the most part expressed the air of a party which has lost its way. A Party in retreat.

But most telling were May’s two policy announcements that were heralded as the most important: cash for social housing and a cap on utility bills. Both, of course, pinched from Labour.

Social Housing

The £1.2bn announced for social housing sounds a lot of money. But when it was admitted that would only fund 5,000 new houses a year, it was quickly seen as underwhelming. Nearly 40,000 new social houses were built in the year 2010 when David Cameron took over from Gordon Brown. That’s now down to about 6,000. So May’s promise just takes us a tiny way back to where we were. But it’s important as an admission that the housing market is not meeting people’s needs.

Miliband revisited!

The second policy announcement, a cap on utility bills, is also an admission of market failure. And here, of course, May is channelling her inner Ed Miliband. When he, as Labour leader, proposed more-or-less the same thing, he was hounded down by the usual suspects in the press and by his Tory opponents. Where’s the criticism now? Once again, markets are in retreat.

And yet, just a few days before, May had sung the praises of free markets. The Tories really are all over the place on this, in contrast to Labour’s consistency.

That Speech

Supply your own caption!

I couldn’t finish without a word about May’s speech at Conference. I’ve written in the past about the guilty pleasure of schadenfreude. As (I hope!) a decent human being, I couldn’t help feeling sorry for the woman about her cough. But I did laugh a lot at the falling letter F: the “F off, everyone” implications are too great! But the metaphor for a crumbling Party and a failing ideology is all too obvious. Perhaps this was the moment when the old economic orthodoxy was – without a doubt – in retreat.

I have been watching and waiting, with increasing despair, for an end to a disastrous 35-year experiment with our lives. I’m talking of the economic policies which have dominated our politics since Thatcher and Reagan began their counter-revolution in the 1980s. At last, in Jeremy Corbyn, I see the first signs that this may, at long last, be happening.

The sociopathic approach to economics which I call Free Market Fundamentalism collapsed and failed, big time, in 2007-8, initially in the USA, spreading to other western economies. The UK was particularly vulnerable owing to our over-dependence on financial services and the consequential destruction of most of our manufacturing industry. Ten years on, we are yet to change course.

The Evidence

And yet, the evidence of the collapse of the old order is everywhere to see:

80 dead and 200 families homeless in the aftermath of the Grenfell Tower fire. It’s the natural consequence of contempt for the poor – yes, I do mean you, Kensington and Chelsea Council, and many more besides. And a disdain for proper regulation, in this case mainly fire regulations.

400,000-plus passengers left high and dry following mass cancellations of Ryanair flights. This is caused by a combination of contemptuous treatment of passengers as cash cows and disgruntled pilots with inferior working conditions.

The loss of Uber’s operating licence in London, for failure to take passenger safety seriously and using unethical but (just) legal methods to deny basic employment rights to its drivers. This threatens inconvenience to users and a loss of thousands of jobs after Uber’s unfair business practices decimated the traditional minicab businesses.

Young renters paying 3 times as much as their grandparents did at the same age for a roof over their heads, as a direct result of decades of a disastrously marketised and deregulated – and self-evidently dysfunctional – housing policy.

The rise and rise of the use of “inspiring” (thank you, Jacob Rees-Mogg) food banks, the majority of users from working households. This follows the introduction of vindictive changes of policy in the treatment of benefit claimants.

A highly fragmented and confusing education system with demoralised teachers as a result of a false belief that the mantra of competition is appropriate in the particular case of educating our future citizens.

Shocking and illegal levels of air pollution in our major cities, concentrated in poorer areas, as a result of under-regulation of vehicle emissions and failure to stand up to vested interests.

Rises in energy costs and rail fares and under-investment in the future resilience of our basic infrastructure, through privatisation of key areas of our economy where markets and competition simply don’t work.

A worrying rise in intolerance, abuse and violence against minorities, women and political opponents. This follows decades of encouragement from newspapers owned by tax-dodging tax exiles. But it’s now amplified by the more lunatic fringes of social media and the blogosphere.

There is a clear chain of causation which links each of these outcomes back to the FMF dogma, which can be summarised as “greed is good”.

May and Corbyn

May at BoE

The Tories seem blind to all this, too busy tearing themselves apart over Britain and the EU to notice. Theresa May’s speech today, commemorating 20 years of Bank of England independence, was largely a paean to free markets. To be fair, she did mention the importance of proper regulation. But she has been saying this for some time, and it’s all words, no deeds. You get the impression that her weakened position as leader can only be sustained by continuing to bow to the gods of the status quo.

Corbyn at Brighton

By way of contrast, Jeremy Corbyn’s closing speech to the Labour Party Conference yesterday recognises that times have changed. And that only Labour has caught the mood. He is clearly determined to embrace the break from the follies of the last three and a half decades and bring us back to the true mainstream. I disagree totally with Corbyn’s critics who try to paint him as some left-wing extremist. Labour’s policy announcements are classic mainstream social democracy. Most of his policies, e.g. rent controls and public ownership of key infrastructure industries, are everyday mainstream politics in other European countries. And, as I have arguing in this blog for over two years, social democracy is a perfect fit for how human beings – psychologically healthy ones at least – actually think.

I hope that Corbyn and colleagues can continue to surf the wave of the realisation that things must change. And about time!

Arguably, the most successful soundbite of last year’s EU referendum campaign was “take back control”, used by the Leave team. It was delusional, of course, based upon the ridiculous idea that Little Britain could be master of its own destiny outside the EU. The realpolitik of 21st century capitalism means that the mega-rich and multinational corporations are free to move capital – and jobs – around the globe. This makes pure fantasy the idea that one medium-sized country can be in control. Standing together with like-minded countries in a bloc like the EU gives some chance of the needs of the people winning – sometimes – against the rich, powerful and footloose. On our own, forget it.

But the idea – and the phrase – caught the imagination of many, assuming they didn’t think too deeply about it.

Ironically, one year on from the referendum, the idea of taking back control – in a different sense from before – is really beginning to catch on. And, this time, it’s a development of which I approve. Two recent events best illustrate my point.

The 2017 General Election

Once again, the pollsters got it wrong. The Tories’ loss of overall majority came as a surprise and, this time, a pleasant one for me. (The shocks of 1970, 1992 and 2015 were three times too many for one lifetime!) There genuinely seem to be signs of change. Specifically, I mean signs that more and more voters are seeing the Tories and their austerity agenda in its true colours: as a way of reinforcing the power and wealth of a minority at the expense of everyone else.

People are beginning to see the value of the public sphere: the schools, hospitals, police, firefighters, public infrastructure, clean air, enforcement of reasonable regulations for safety in employment, and many more. It extends to an appreciation of the longer-term strategic view that public ownership can give to areas such as blue-sky R&D and in the energy sector.

For three and a half decades, government and economists have asserted the supremacy of free market fundamentalism. They assert that free markets, unfettered by government interference, will produce the best of all possible outcomes. For the poor, their concerns and fears are vilified or ignored. At long last, an increasing number of people see that assertion for what it is: a lie.

They can see with their own eyes that the average worker is still worse off than before the 2007-8 global financial crash. They can see the rise of low quality, insecure jobs and the sham self-employment. They see ruthless employers increasingly treating their workforce with contempt. Too many people feel they have no control over their lives. Job insecurity means they cannot make sensible plans for the future, about basic matters such as housing and starting a family. For the rich, every whim and opinion is indulged and flattered.

The recent general election result showed that more people have seen through the Tories’ lies. Corbyn’s Labour Party finally gave them a real choice: a chance to get back some control. Emphasis on workers’ rights and the renationalisation of railways and utilities is seen to make sense. Private utilities casually rip off their customers – their nationalised forebears never exploited them in that way.

The Grenfell Tower Tragedy

And then came that most unimaginably awful, utterly avoidable tragedy: the Grenfell Tower fire. Four weeks on, those who have lost their homes and those who have lost loved ones still haven’t had their questions answered. Still the authorities, above all Kensington and Chelsea Council, are failing in their most basic obligations to the residents. Most of the support and help for practical, emotional and psychological issues still seem to be given by volunteers and community organisations. Yet Kensington and Chelsea is the UK’s richest authority, with nearly £300m in its reserves. The total breakdown of trust between the state and the citizens of the area is palpably raw and tragic. The Grenfell residents aren’t being given even the basic answers to help begin a grieving process and to rebuild their lives. The lack of control they have over their present and future lives screams out every minute of every ghastly day.

Out of Control

Whilst in no way comparable, I remember clearly the moment I found out my first wife, in her mid-40s, had been diagnosed with cancer. There was an overwhelming sense that our lives had, very suddenly, got totally out of control. Over the following few days, through our own research and with good support from medical staff answering our many questions, we began to feel better able to cope. The cancer hadn’t gone away, but we had more information to begin to make sense of it all and gain a feeling of control once again.

It would be simply wrong, impertinent and insulting to the Grenfell victims to say I know how they feel. But it is, after all, a defining feature of being human that we try, however inadequately, to empathise with those who are suffering. All I can say with any certainty is that it must be massively, massively worse than what I went through – unimaginably so.

A Turning Point?

It feels like the Grenfell fire and its aftermath is a turning point: I really, really hope it is. Grenfell, or something like it, is what happens after thirty-five years of inhumane economic policy, treating humans simply as economic units. And, as economic units, the rich and powerful are treated with utmost respect; the poor and vulnerable with utmost contempt. I sense that people really have had enough, at last.

The hope now is that we can be led by people with the vision to plot a new path to the future. The Labour Party manifesto for the recent election was a good start. Jeremy Corbyn seems to have found his feet. He clearly recognises that, if everyone is to “take back control” of their lives, most of us, at some time need the state to be there to lend a helping hand. This help takes many forms: benefits, doctors, nurses, firefighters, a decent job with a predictable wage or basic needs like gas and electricity from an organisation that doesn’t try to rip you off all the time.

The Tories won’t get us there. Several members of May’s cabinet are professed admirers of Ayn Rand and have called her most famous novel an “inspiration” – here’s one example. Free Market Fundamentalism, that cruel and heartless creed of greed, is the natural brainchild of Rand’s cold-hearted and false assumptions about human behaviour. It must stop. All the people of Britain, poor and rich, must be given the opportunity to take back control of their lives. Starting now.

We are still recovering, painfully slowly, from the global economic crash of 2007-8. Average real pay is still below pre-crash levels, with only Greece performing more badly than the UK on this measure within Europe. I fear we now have the conditions in place to sleepwalk into the next crash. The 2007-8 crash started in the USA, the trigger attributed to the collapse in the so-called “sub-prime” mortgage lending market. In other words, mortgage companies lent money to people who, increasingly, were unlikely to keep up with the payments. The Tories under Cameron and Osborne seem to have successfully (and unfairly) laid the blame on the Labour Party, on whose watch the crash occurred.

Assuming the Conservatives win on June 8th, I reckon there is a greater than fifty-fifty chance the next crash will happen on Theresa May’s watch. Only this time, the causes will be more home-grown. We don’t have the same set of circumstances as we had just before the last crash, but we have some very similar problems – and the lessons of the last crash have not been learned.

Household Debt

The level of debt in UK households has been climbing to a record high whilst savings have fallen to a record low. The number of County Court Judgements (CCJs) against debtors has hit a ten year high. And now real wages are falling again. The FT reported this last week, along with the assessment that the last ten years have been the worst for wage earners since the Napoleonic Wars 200 years ago. The economy as a whole has been growing at less than half the rate it did for the first 30 years after the war, when economic policies very similar to those in Labour’s manifesto were followed by Tory and Labour governments alike. Such growth as there has been in the last decade has been snuffled up by the richest 1% of the population – leaving the rest of us worse off than a decade ago. And that growth has largely been funded by more personal borrowing.

Sub-Prime 2.1: Credit Cards

On top of this, there are strong indications that banks and other financial institutions are finding new ways to lend recklessly. Low, or zero, introductory interest rates are luring more people into the credit card habit. As well as the increasing risk of default, companies have been flattering their accounts by a new piece of creative accountancy. They are including future profits from when the introductory rate ends in their current income and so are flattering their financial position. This practice is very similar to an accounting trick used by Tesco for which it was fined £129m by the Financial Conduct Authority, plus a bill of £85m compensation to suppliers.

The risk here is that finance companies engaging in this practice are giving a false (and flattering) account of their financial position.

Sub-Prime 2.2: Car Financing

Over the past few years, motor traders have frequently been in the news – good news – for announcing record car sales. Much of the growth can be attributed to a new way of financing the cost of the car purchase, known as “personal contract plans”. An article here includes a quote from a finance expert that “Borrowing is a very bad idea when it is done against a depreciating asset … such as a car,” adding that there was a “serious level of fragility built into the system”. Something similar is happening in the US, prompting the article Will Cars Be the Death of Us This Time?

Don’t be surprised if the wheels drop off of this wheeze sometime soon.

UK’s Unique Vulnerability

Add to all this, the UK is uniquely vulnerable to disturbances in the global financial system. In my 2015 post Two Gamblers and a Pint of Lager, I explained just how exposed the UK is, with our extreme over-dependence on financial services. With 1% of the global population, we have 37% of the most risky type of financial transactions. Total City trading gambles our entire annual national income every day and a quarter. The right word for such behaviour is “madness”.

So, all it would take is a bit of a shock to the system. If the opinion polls are correct, Britain will vote on 8th June for the maximum possible risk of the biggest shock to our finances since at least the 1970s, and probably since the Second World War. I’m talking about the distinct possibility of the UK crashing out of the EU without a trade deal. Prime Minister May has already ruled out staying in the single market by her obsession on immigration. Add to that May’s character: stubborn, inflexible and with strong control-freak tendencies – look at how the Tory election campaign is being hyper-controlled by a small team of close advisers. Together with her lack of understanding of European sensitivities, egged on by a rabid right-wing press, a vote for the Tories is the maximum risk choice.

Have you held a new five pound note in your hand yet and taken a good look at it? I have: in a word, YUK! I have no problem with the fact it’s a polymer note. The Australians have had plastic money for over twenty years and other nations more recently also. My quibble is the design.

New Fiver

The images above, as seen on my computer screen, are flattering: in real life, the contrast is reduced and the overall impression is of a blue-grey sludge, particularly on the font. Think of some mould that’s grown over something in the fridge you should have thrown out weeks ago. Or think of some image or sign left out in the sun and the picture and colours have faded.

And just look at the typography and calligraphy. The bold “5” has disappeared, as it did when the £20 note was last changed. That, the fussy typeface and the low contrast all make life more difficult for thousands of visually impaired people. All those squiggles look like the work of a very bored six year old in a school writing lesson.

Apart, of course, from the faces of the two individuals portrayed, the note looks like it could have been designed at any time between the fifteenth century and the 1940s. In fact it’s worse than that, as early 20th century movements such as art deco had a lasting and wide impact on modern design principles.

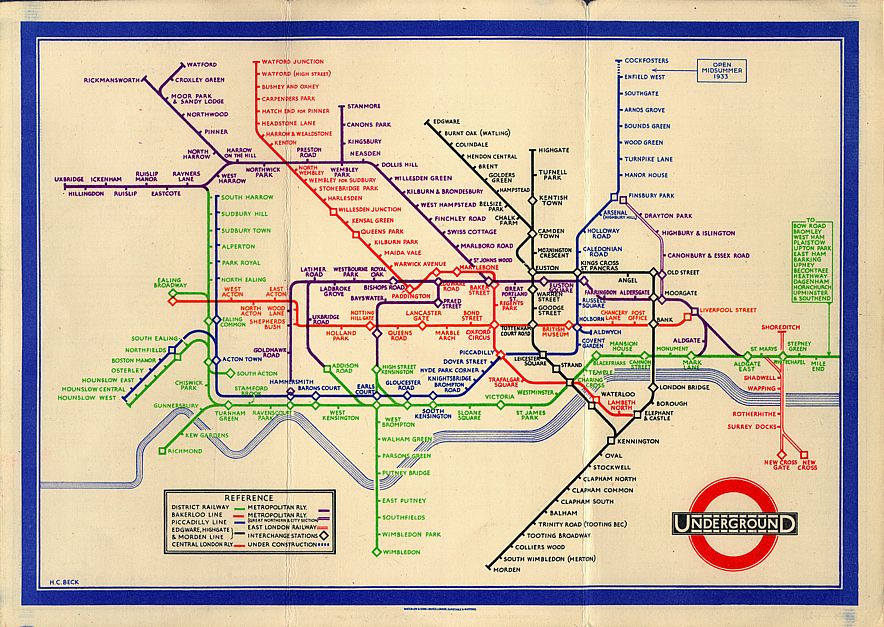

Good Design

The UK is a world leader in good design. In diverse fields such as the arts, architecture and everyday household objects, we’re world class. For example, the London Tube Map, first published in the 1930s, is a design classic. The Design Council has been doing an excellent job for 70 years encouraging good design and new designers. It estimates that’s worth £71 billion a year, or 7% of the UK’s income (Gross Value Added to be technical). That’s nearly as much as the much valued (by politicians) financial services sector.

A Design Classic

Despite some internet research, I’ve not yet found any information telling me who was responsible for the design: certainly, the Design Council’s website search facility draws a blank. Whoever they were, they seem to be trapped in a time-warp bubble which significantly pre-dates the 21st century. The Bank of England does have a “Banknote Character Advisory Committee” (yes, really!) who are responsible for advising on which people’s faces appear on new banknotes. This Committee is reasonably diverse in its membership, which offers some hope. But for the actual design, does anyone know?

Oh, and one last thing: it should have been a coin.

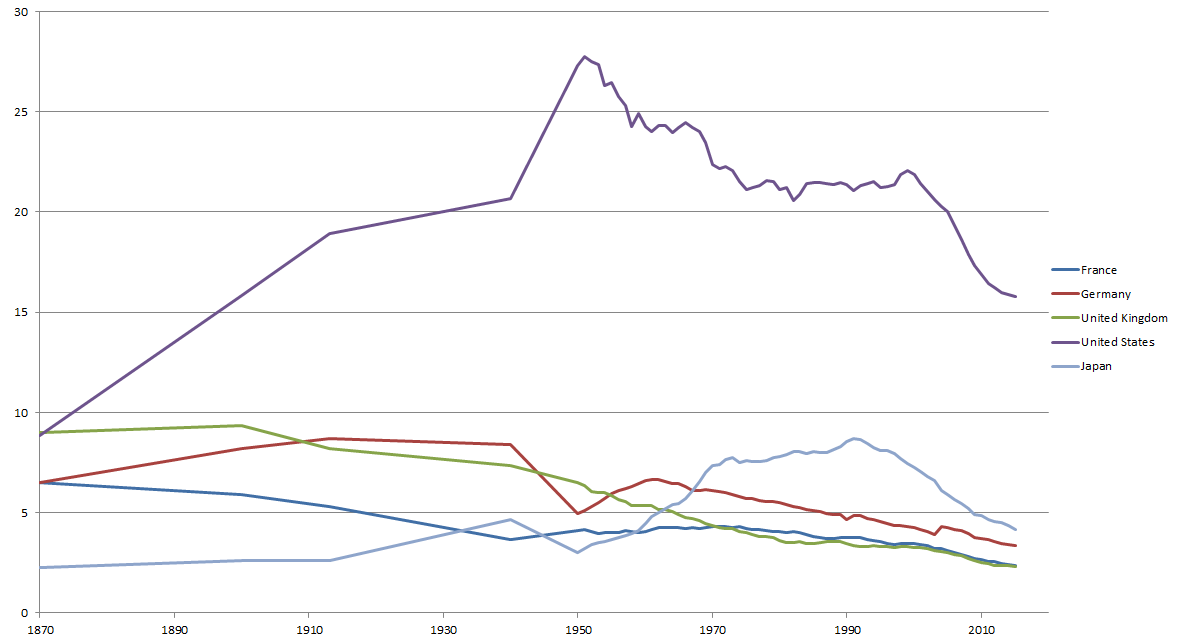

Britain has been in decline for 140 years. By this, I mean that it has been in relative economic decline: relative, that is, to its main rivals and to the overall global economy. The graph below shows Britain (in green) and other countries’ position since 1870, as a percentage of total global income (GDP). The UK had 9% of all global income in 1870, at the height of the British Empire. Today, this has fallen to under 2.4%. The green line shows a remorseless slide downwards.

Share of global GDP

The last 20 years or so shows that Britain shares this downward trend with the other countries shown. The main reason is the recent rise in the economies of China above all and, to a lesser degree, India, Brazil and Russia.

Referendum Effect

I have previously reported that the UK slipped from 5th to 6th largest economy on the day after the EU referendum. This was the result of the instant drop in the value of sterling. Last week, the Bank of England took action to boost growth by cutting interest rates to the lowest level ever seen. Other measures were announced, including more “quantitative easing” (a.k.a. printing money), to try to stave off a new recession.

At the same time, the Bank of England revised its forecast of growth of the UK economy. For next year, the downward revision from 2.3% growth to only 0.8% marks the greatest ever downward revision by the Bank in its history. A further smaller downward drop was made to the growth forecast for the following year. This will make our national income £45 billion lower in 2018 than expected pre-referendum. Once again, our £7bn cost of EU membership looks a real bargain.

Former Chancellor George Osborne has a fetish: it’s called austerity. On taking office in 2010, he tipped the UK back into recession by a combination of poor policy and some foolish talk. Of the latter, his false assertion that the UK economy was like Greece’s was perhaps the most foolish. George has been sacked, but he may yet have helped to make his remarks come true – one day. Under his watch, UK productivity growth has been zero. Our relative position is the worst ever. Our productivity is now 18 percentage points below the average for the world’s major economies (G7). That alone is a strong indicator that Britain will continue to lag behind in economic growth.

The new chancellor seems to be taking his time to learn his brief. The lack of action from him contrasts with the more decisive actions from Carney and the Bank. Expert opinion is that both sets of action are needed. Even that will probably not be enough to repair the damage cause by the referendum result.

“We’re All Doomed!”

Added to all this is Britain’s lopsided economy, with its over-reliance on financial services. With the failed free market fundamentalism still dominant in the UK and at the ECB, Britain is uniquely vulnerable. A characteristic of FMF policies is the increasing likelihood, over time, of bigger and bigger economic crashes of the type last seen in 2007-8. Remember the figures: 1%, 2.5%, 37% from my earlier post Two Gamblers and a Pint of Lager. With 1% of global population and 2.5% of global income, the UK engages in 37% of the world’s speculative financial transactions. These are the kind that are most destructive to the “real” economy, according to the IMF. When the next big crash comes, we’ll be hit hardest.

Terminal Decline?

So, in this context, the referendum result looks to me like the firing shot in the final phase of Britain’s long fall from imperial glory (or hubris): our terminal decline to rancour, intolerance, introspection and global irrelevance. Welcome to the future of Britain!

Readers of my earlier posts will know that I fundamentally disagree with the prevailing economic policy I call “free market fundamentalism”. Well, a new report by the “High Church” of economic policy, the International Monetary Fund, gives me some slight hope for a change. The report was written by Ostri, Loungani and Furceri of the IMF’s research department. Its sub-headline states “Instead of delivering growth, some neoliberal policies have increased inequality, in turn jeopardizing durable expansion”.

To be fair to the authors, they do acknowledge that some reforms under the neoliberal agenda have been beneficial. For example, the increase in global trade and foreign investment has “rescued millions from abject poverty” and helped to transfer skills to developing countries. But the report highlights two specific areas with a far more critical eye.

Free Movement of Capital

The first area concerns the widely adopted policy of removing restrictions on the movement of capital around the world. Proponents of this policy state this enables capital to move to where it will be most productive. But in practice, a great many of these capital flows take the form of portfolio investment or speculative trading. There is no discernible benefit in terms of growth from such flows. What’s worse, there is strong evidence that it leads to much greater instability: “boom and bust”. This instability, in turn, damages growth and hurts poorer people most. In other words, it decreases stability and increases inequality. Increased inequality, in its turn, reduces growth. (See my earlier post Inequality Damages Your Wealth.)

The upshot is that freedom of capital movement does more harm than good.

Incidentally, it’s worth noticing the lopsided nature of Free Market Fundamentalism policy in this respect. Capital is allowed to flow freely across borders; people are not. (Look at the frenzy that the Brexiteers – über-free marketeers to a man – are whipping up about free movement of labour in the EU.) The link to inequality is obvious. The rich have capital to spare to move around the world. The poor have just their own skills, their own labour. Extra freedoms for the former and none for the latter are bound to increase inequality in the longer term.

Austerity

Austerity policy is everywhere: it’s been George Osborne’s mantra for the last six years. Its stated aim of reducing government debt is always used as a cover to shrink the state. The report concedes that reduced levels of debt, all other things being equal, are helpful to growth. But the means of getting there is more damaging to growth than the benefits. It concludes: “Faced with a choice between living with the higher debt—allowing the debt ratio to decline organically through growth—or deliberately running budgetary surpluses to reduce the debt, governments with ample fiscal space will do better by living with the debt.” (The report states that the UK is a country “with ample fiscal space”.)

Two International Institutions

In summary, the IMF said that the discredited policies did not boost growth, that the downside in terms of increased inequality was “prominent” and this in turn damaged growth.

As well as the IMF, the OECD, the other main respected international body on economic matters, also weighed into the subject in February. Its report recommended that countries like Britain should reduce austerity and invest more public money in infrastructure.

The IMF report ends with these words: “Policymakers, and institutions like the IMF that advise them, must be guided not by faith, but by evidence of what has worked.” Quite: the FMF sacred cow is overdue for slaughter.

Sadly, the continuing misfortune for Britain is that we have a government, elected on just 37% of the popular vote, but over 50% funded by City organisations and finance companies – many specialising in the corrosive, speculative end of the business. Cameron and company will continue to take the City’s interests as the same as the nation’s. (My earlier post, The City: Paragon or Parasite? shows those interests are not the same – and more like opposites.) The necessary lessons from this new understanding will be learnt very belatedly, if at all.

Light…

But the good news is that the two main economic institutions in the world are now seriously questioning the orthodoxy of the past 35 years’ economic policies. There is a glimmer of hope that, one day, even the British government will realise the errors of its ways. Let’s hope we don’t have to wait for the next crash before things start to change.